{kind=link}

[ad_1]

Wall Avenue obtained a actuality verify on Tuesday, with hotter-than-estimated inflation knowledge triggering a slide in each shares and bonds.

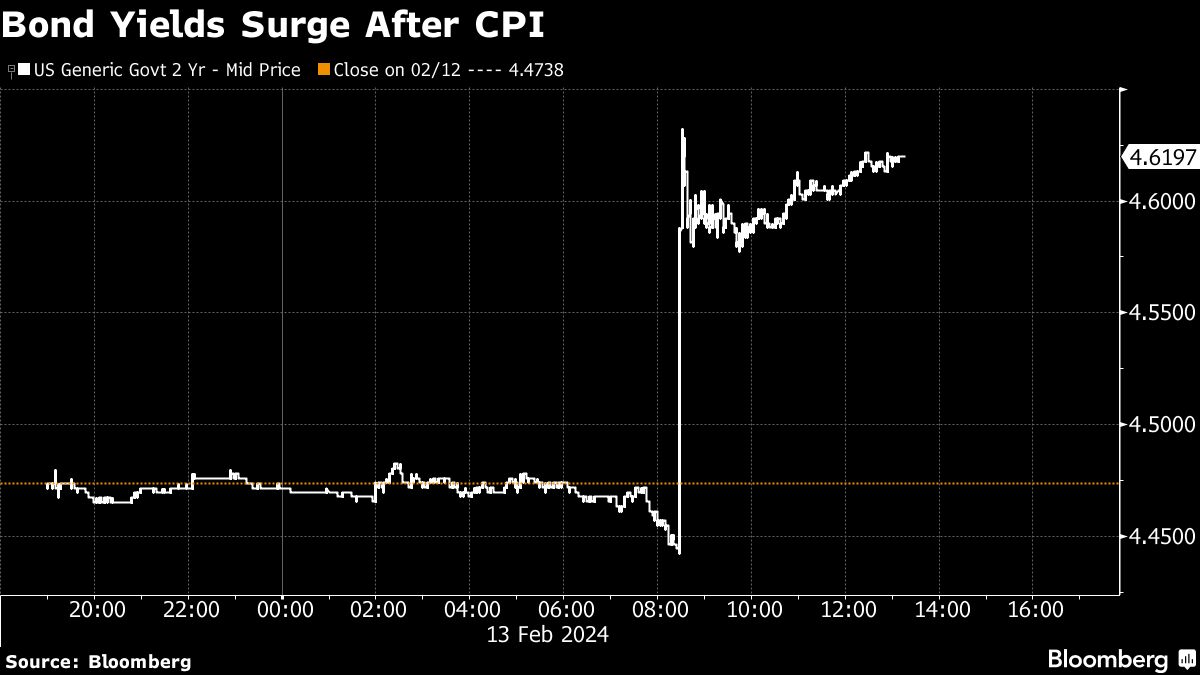

Equities moved away from their all-time highs after the core shopper value index topped estimates and climbed probably the most in eight months. Treasurys offered off, with two-year yields hitting the best since earlier than the December central financial institution “pivot.”

Swap merchants all however deserted expectations for a Fed reduce earlier than July. And a measure of perceived danger within the U.S. investment-grade company bond market soared — with three issuers getting sidelined.

The CPI knowledge got here as a disappointment for traders after a latest downdraft in value pressures that helped construct expectations for charge cuts this yr. The numbers additionally gave credence to the wait-and-see strategy highlighted by Jerome Powell and a refrain of Fed audio system.

“If Powell and different Fed members hadn’t already thrown chilly water on the prospects for a March charge reduce a number of weeks in the past, at present’s CPI report might need finished that,” stated Jason Pleasure at Glenmede. “Proof of still-sticky providers inflation is probably going to offer the Fed pause earlier than slicing charges too rapidly.”

Pleasure says charge cuts are doubtless nonetheless on the desk for this yr, however they could start later than the market could also be anticipating.

The S&P 500 fell beneath 5,000, heading for its worst CPI day since September 2022. Charge-sensitive shares like homebuilders and banks sank, whereas Microsoft Corp. led losses in megacaps.

U.S. 10-year yields climbed 10 foundation factors to 4.28% — set for the best since November. The greenback rose and gold fell beneath $2,000.

“Whereas the door for a March reduce had already been successfully shut given the latest Fed commentary and the roles studies, the Fed has now locked the door and misplaced the important thing,” stated Greg Wilensky at Janus Henderson Traders.

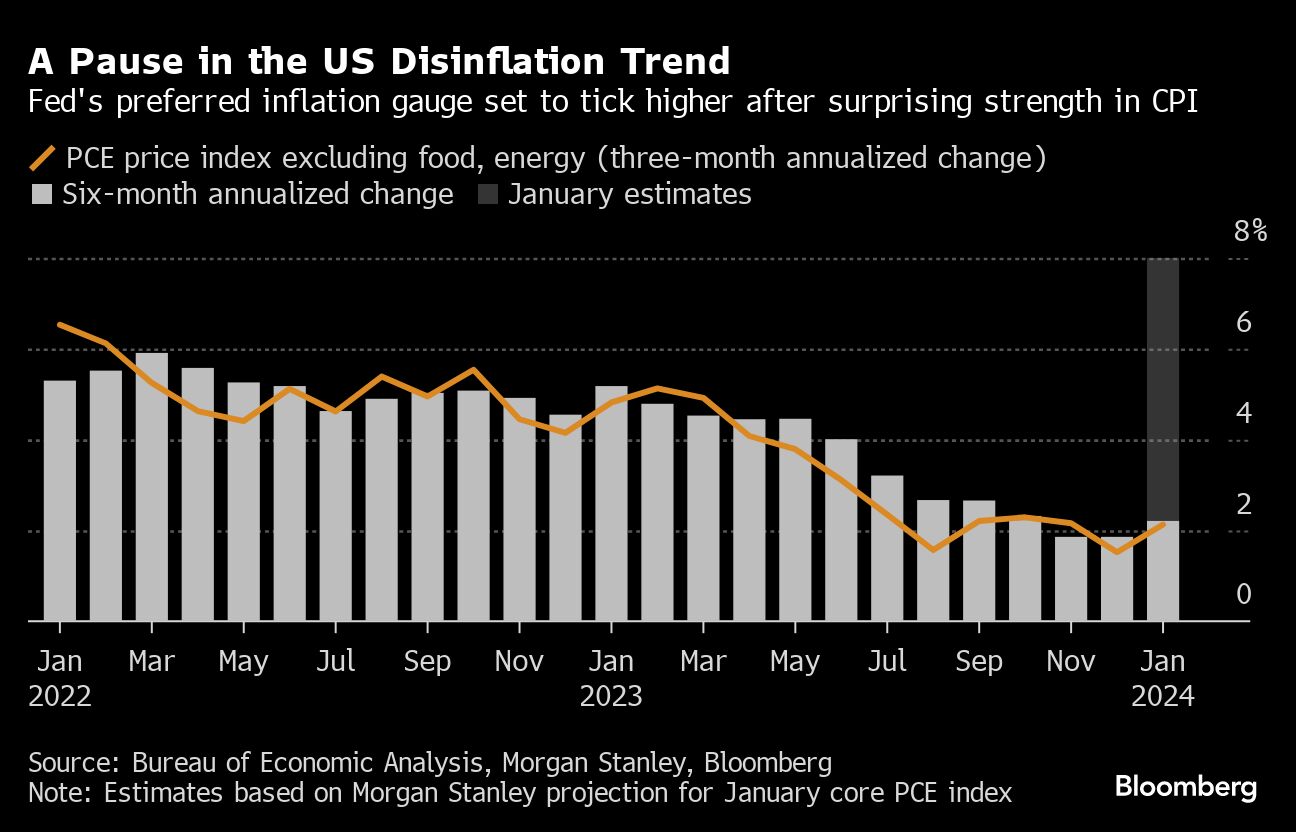

A lot of the unanticipated improve in CPI was concentrated in what appears to be like like a “noisy leap” in House owners’ Equal Lease (OER) — a shelter value indicator, based on Tiffany Wilding at Pacific Funding Administration Co. Whereas that may doubtless revert, the main points have been in line with the Fed having a “final mile downside” — and never slicing charges till midyear or later, she added.

Swap contracts referencing Fed coverage conferences — which as not too long ago as mid-January absolutely priced in a charge reduce in Might and 175 foundation factors of easing by the tip of the yr — have been roiled. The chances of a Might reduce dropped to about 36% from about 64% earlier than the inflation knowledge, with fewer than 100 foundation factors anticipated this yr.

Fed officers are being confirmed proper of their “take it gradual” strategy, based on Russell Worth at Ameriprise. He says the primary charge reduce may come as early as June — however it may simply be July and not using a materials enchancment in near-term inflation tendencies.

The January CPI report is a reminder that inflation is a troublesome, not-well-understood downside that doesn’t transfer in a straight line, based on Chris Zaccarelli at Impartial Advisor Alliance.

“Bonds are too costly if inflation remains to be an issue and the inventory market can’t maintain rallying if charges are going to be higher-for-longer — particularly if the idea that the Fed is totally finished elevating charges is wrong,” he added.

Previous to Tuesday’s knowledge, strategists at Citigroup Inc. famous that what was lacking was merchants hedging the chance of a really temporary easing cycle adopted by charge will increase shortly thereafter.

[ad_2]